|

|

| |

Our Two Cents

with TMFG

Your Monthly Update on Everything Going On in Your TMFG Financial World All in One Place. Ask TMFG videos, Our Podcast, Fun and Interesting Articles, Updates, Events and More.

|

|

| |

Happy New Year!

|

| |

|

Announcements Announcements

A special message from the TMFG team

The McClelland Financial Group

Holiday Toy Drive

2022 McClelland CP24 Chum Wish Foundation raised $1600 in toys and monetary donations for children in need this holiday season. A big thanks to all our clients for making this possible.

|

| |

Holiday Arrangement and

Cocktail Event was a smash!

|

| |

In case you missed

The EV Cars Event

Watch the video here

|

| |

|

FINANCE FINANCE

Light Read – Useful and Relevant

Finance

A Volatile Year As Expected

A lot has gone on in our market since January 1st, 2022. We have had a war between Russia and Ukraine and experienced the highest inflation in Canada since 1983; we have experienced a very aggressive interest rate hike with the highest rates since the Financial Crisis in 2008, all while our society gets back to "normal" after COVID-19.

The events listed above have led to a volatile marketplace in 2022. But is that out of the ordinary for our markets? When we reflect on each of our years, we can come up with negative news stories that impacted our needs, and we can also come up with positive news. Volatility is a regular part of the investing process; accepting volatility will mean a much more enjoyable investment experience.

The chart below illustrates the last 20 years in the US market, a period where we ended with 17 positive calendar year returns. There was not one year we had where the market remained positive from January 1st to December 31st. That means in the last 20 years, the US stock market returns were negative at some point during each calendar year.

This year has been no different. 2022 will be remembered as a negative year in our market, but we have seen a drastic turnaround in the last three months alone. Let's look at the DFA Global Equity Portfolio; for example, this is an all-stock portfolio invested in different countries and industries worldwide.

As of September 30th, 2022, this portfolio had a year-to-date return of -14.34%.

From the period of October 1st, 2022, to December 13th, 2022, that same fund had a rate of return of 11.84%.

Therefore, leaving the total year-to-date return of the fund at -4.2%. Which is a significant improvement in under three months.

So, while this year will be remembered as a "negative year" by most investors, I recognize it as a volatile year, no different than any of our past 20 years in the market. While the negative news articles are the ones that get the most attention, let's shed some light on positive financial news that is going unnoticed and is playing a role in the market's recovery in the past three months.

Positive news:

Supply Chain is recovering - Oxford Economics in the UK developed a measure for Supply Chain Strain. According to their metrics, the supply chain has improved significantly over the past several months.

Inflation is declining - With the supply chain recovering and interest rates increasing, inflation has begun to decline in Canada and the US. We still have a way to get back to our normal inflationary levels, but we are heading in the right direction.

Unemployment is low - In Canada and the US, unemployment numbers are historically low, which has improved dramatically since coming out of the pandemic.

The most common question from our clients is, what do you expect next year? Well, I think you can continue to expect volatility. You can continue to expect positive and negative news to impact our markets. But most importantly, if you stay committed to your financial plan, Invest in a globally diversified portfolio, rebalance where necessary, and accept the volatility we will continue to face, you can expect successful markets in your future.

|

John Iaconetti B.A.S., Spec. Hons. Administrative Studies (Finance)

Financial Advisor

The McClelland Financial Group of Assante Capital Management Ltd.

|

|

| |

|

|

| |

|

|

| |

|

FINANCE

Light Read – Useful and Relevant

Finance

Are RRSPs actually a good thing?

Well, it depends on who you ask. In order to answer the question, we have to establish what an RRSP is and what the benefits are. In short, an RRSP stands for Registered Retirement Savings Plan. Created in 1957, the RRSP is a type of investment account that provides income tax deferral opportunities to Canadians who contribute into them. The CRA is using this incentive to encourage Canadians to save for their eventual retirement when they’ll have to rely on more passive sources of income to subsidize their lifestyle.

The initial benefit is provided by the deduction allowed on the amount contributed. This means that the amount of any contributions can be deducted from the total income, resulting in “non-taxed” contributions. Typically, these contributions are made during the taxpayer’s highest income years. Due to Canada’s graduated tax rates, the most benefit is gained by making contributions when the income is highest.

The delayed benefit is the tax-deferral allowed on investment income earned while invested within the RRSP. Depending on the type of investment (i.e. stocks, bonds, mutual funds, cash, etc.), the income generated – whether it’s dividends, interest, or capital gains – is not taxable in the year that it is earned. Conceptually, the investment growth should compound faster given that it is not encumbered by tax.

Understanding the two main benefits is the first step in determining the usefulness of an RRSP. The second step is determining what your income situation will be when you “retire”. This is important because withdrawals made from the RRSP are taxable. Your income tax rate will be determined by how much income you have in the year. Again, given the graduated tax rates in Canada, the less income you have means a lower tax rate payable.

Ideally, a Canadian taxpayer will make their RRSP contributions in years when their tax rate is higher than when they will start withdrawing. Typically, a Canadian taxpayer will have less income in their retirement years than when they are working. By utilizing the RRSP, a Canadian can defer the tax calculation on income from high-income years to low-income years – or from high tax rate years to low tax rate years.

This concept becomes an issue when retirees have the same amount (or more) of income in their retirement years as they did in the working years. The simplest example would be employees who have Defined Benefit Pension Plans. These retirees worked for employers who provided the opportunity for a life-time income (typically a percentage of the amount that they earned annually, depending on the length of time of service). For example, a federal government employee who receives a pension of 60% of their working salary could make up the other 40% with government benefits (i.e. CPP, OAS, etc.), business income, investment income, RRSP income, or rental income (depending on how savvy they were with other investments). That is not to say that Canadians with a Defined Benefit Pension Plan shouldn’t contribute into RRSPs. These Canadians just have to be more mindful of their expected retirement income given that they will be starting at a higher amount due to their pension.

At the end of the day, paying income tax is part of being a Canadian. If you pay tax, it means that you have income. The challenge is working within the rules set by the CRA in order to reduce your taxes payable. The RRSP is one of the tools provided. Speak with your TMFG advisor for additional questions or clarification.

|

Carlo Cansino FMA, FCSI, CFP®

Senior Financial Planner

The McClelland Financial Group of Assante Capital Management Ltd.

|

|

| |

|

FUN CHARTS FUN CHARTS

Fun and inventive ways to see interesting ideas!

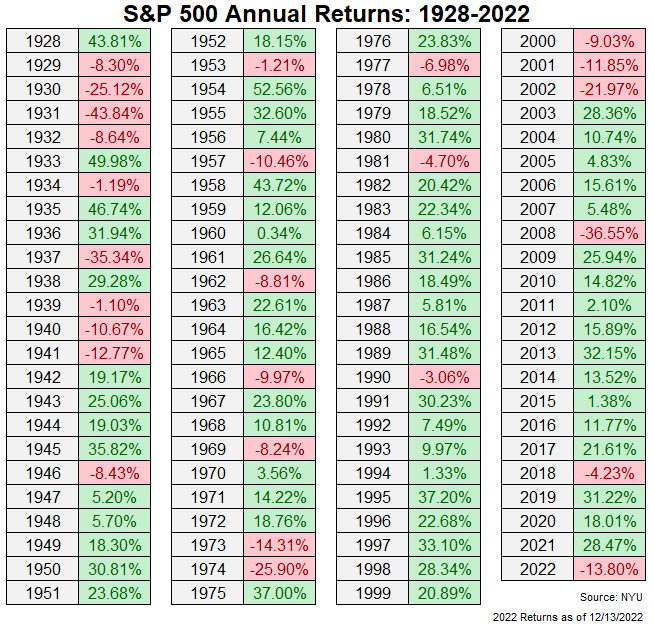

S&P 500 Annual Returns: 1928-2022

View Enlarged Image

Source: NYU

|

| |

|

| |

|

THINK SMART

THINK SMART

Podcast – Listen to Mike and Rob and their latest thoughts and industry insights

Think Smart

The Disengaged Spouse

Evidence shows that women outpace men in lifespan by a minimum of five years. Yet we often see that only one partner does all the financial heavy lifting while the other remains disengaged and uninformed. Ensuring that both partners are engaged in understanding their finances is crucial to the future of the surviving spouse. Not only does it provide the arena for developing a shared vision of your plan it allows you to highlight any unforeseen discrepancies. If you consider yourself or your spouse disengaged, it’s not too late. Listen today to Senior Financial Advisors Rob McClelland and Mike Connon to discover your next steps.

LISTEN TO THE LATEST PODCAST

|

| |

Ask TMFG

Should I put my money in an RRSP?

Watch The Latest Videos

|

| |

|

|

|

Assante Capital Management Ltd. is a Member of the Canadian Investor Protection Fund and Investment Industry Regulatory Organization of Canada. This material is provided for general information and is subject to change without

notice. Every effort has been made to compile this material from reliable sources however no warranty can be made as to its accuracy or completeness. Before acting on any of the above, please make sure to see me for individual

financial advice based on your personal circumstances. Insurance products and services are provided through Assante Estate and Insurance Services Inc.

Commissions, trailing commissions, management fees and expenses, may all be associated with mutual fund investments. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Please read the Fund Facts and consult your Assante Advisor before investing.

Certain employees of (TMFG Tax Service) maintain a relationship with Assante Capital Management Ltd. ("Assante") through which they sell investment products. The relationship that they have with Assante does not include tax preparation

services which (TMFG Tax Service) is solely responsible. (TMFG Tax Service) is not associated in any way with Assante, and Assante has no responsibility for the tax preparation services offered by (TMFG Tax Service).

*Please note that a live recording may be conducted at our workshops. Consent will be obtained, should you be captured in the video.

**All personal information will only be used in accordance with your consent, and in compliance with Assante's Privacy Policy.

Let's keep communicating. We value our relationship with you and want to stay in touch, whether it's regarding events or newsletters. In brief, The McClelland Financial Group aims to provide you with information

that is relevant to you. As you are likely aware, on July 1, 2014 Canada's Anti-Spam Legislation (CASL) came into force which requires your consent to receive electronic communications.

If we do not receive an unsubscribe email from you we will continue e-communications under the implied consent provisions under CASL. **

|

|

|