|

|||||||||

|

|

|||||||||

|

|||||||||

|

|||||||||

|

|

|||||||||

GICs – The Good, The Bad and The Ugly Most Canadians are familiar with the term GIC – Guaranteed Investment Certificate. For those that are not, a GIC is a type of fixed-income investment provided by financial institutions. Typically offered in specific terms (1 – 5 years), a GIC guarantees interest payable and the return of principle at the end of the term. The Good - In times of market uncertainty and volatility, GIC owners can rest assured that the principle of their investment is protected. There is no concern that their initial investment amount will decrease in amount. The Bad - Depending on the health of the economy, the interest rate environment may not be very attractive. If interest rates are low, then your investment will not earn a high rate of return. The Ugly - The Consumer Price Index measures changes in the price level of a market basket of consumer goods and services purchased by households. This index is widely accepted as the measurement of inflation for Canada. Why is this important? Simply put, due to inflation, the value of $1 today, will be less or will purchase less goods and services, in the future. The average inflation rate over the last 10 years has been 1.60%. The average 1 year GIC rate over the same period has been 1.37%. By investing your money into a 1 year GIC, you are actually losing value, relative to inflation, over time. Your ability to purchase the same amount of goods and services in the future is lost because your money has not increased at the same rate as prices. The average 5 year GIC rate over the same period has been 2.22%. That said, you are locking your money away for 5 years leaving yourself with limited liquidity and flexibility. Over the short-term, a guaranteed loss of future purchasing power is not a compelling reason to invest in a GIC. Speak with your advisor to discuss investment options that provide the opportunity to outperform inflation.

|

|||||||||

|

|

|||||||||

|

|

|||||||||

InsuranceTravel Insurance Many of our clients enjoy travelling. Whether it be going to your condo in Florida, an exotic photography trip to Africa or travelling across the country to ski in BC, you need to have travel Insurance. |

|||||||||

|

|

|||||||||

|

|

|||||||||

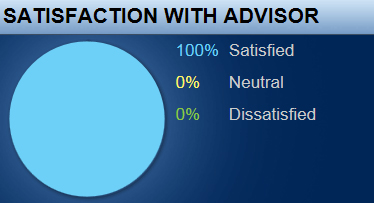

ActiFi Third Party SurveyClient Survey Results - 100% Satisfaction with Advisors

In September of 2015, The McClelland Financial Group of Assante Capital Managment Ltd. sent out a third-party survey to our clients and asked them to rate us on many different levels - see survey here. |

|||||||||

|

|

|||||||||

|

|

|||||||||

|

|||||||||

|

|

|||||||||

|

|||||||||

|

|

|||||||||

|

|

|||||||||

|

|||||||||

|

|

|||||||||

|

Assante Capital Management Ltd. is a member of the Canadian Investor Protection Fund and is registered with the Investment Industry Regulatory Organization of Canada. This material is provided for general information and is subject to change without notice. Every effort has been made to compile this material from reliable sources however no warranty can be made as to its accuracy or completeness. Before acting on any of the above, please make sure to see me for individual financial advice based on your personal circumstances. Insurance products and services are provided through Assante Estate and Insurance Services Inc. The opinions expressed are those of the author and not necessarily those of Assante Capital Management Ltd.

Let's keep communicating. We value our relationship with you and want to stay in touch, whether it's regarding events or newsletters. In brief, The McClelland Financial Group aims to provide you with information that is relevant to you. As you are likely aware, on July 1, 2014 Canada's Anti-Spam Legislation (CASL) came into force which requires your consent to receive electronic communications.

|

|||||||||